Welcome These

presentations are among the best in the industry: honest,

straightforward, and informative. Concepts

are presented using common terms, easy and understandable.

In addition to key points of fact, the author presents

a balanced comparison of benefits and disadvantages so you

can make a sound, confident decision. If you'd like to know

more you can request a quote simply by clicking Here.

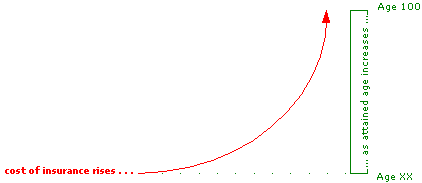

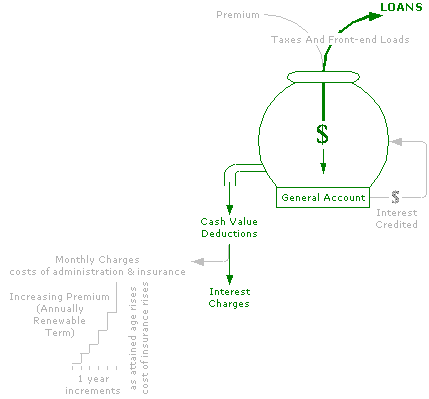

The

cost of insurance is based on several factors, including health,

life-style and age. As the age of the insured rises, the

cost of insurance (sometimes called the mortality charge) also

rises until eventually the cost may become prohibitive.

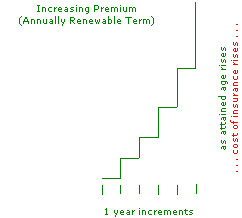

Universal

life is bulit on an annually renewable term product. Each

year the policy will be automatically renewed for another year

without evidence of insurability (no medical check-up required).

However, the amount charged for the annually renewable term product

will increase based on the individual's attained age. The

result is a step-rate premium. As an individual grows older the

step-up becomes greater and greater until eventually the cost

may become prohibitive.

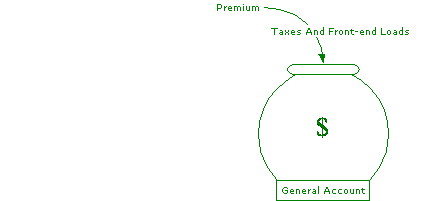

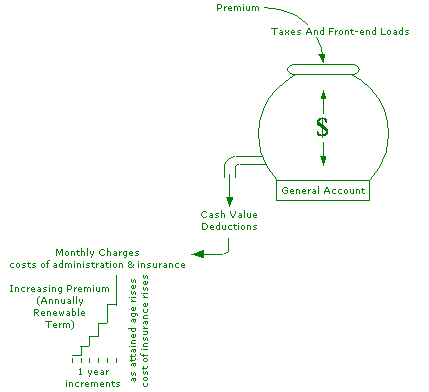

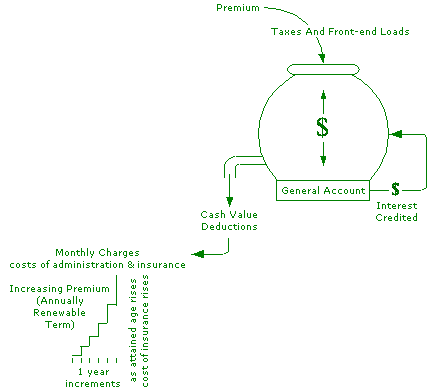

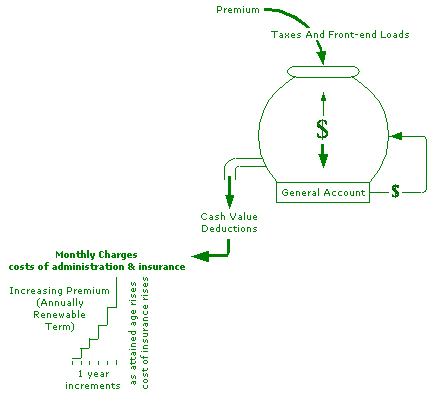

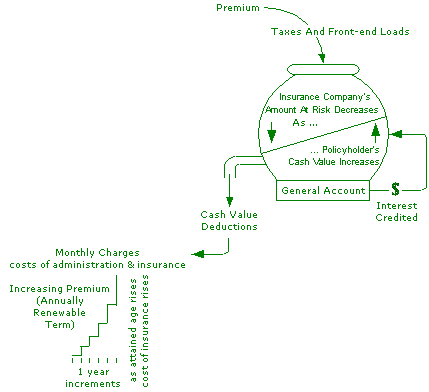

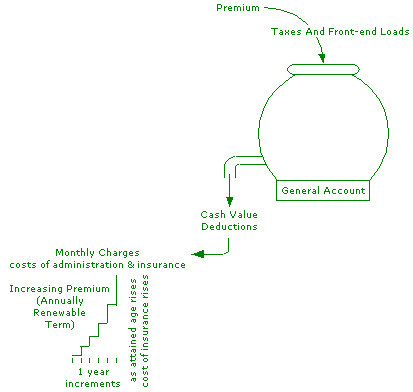

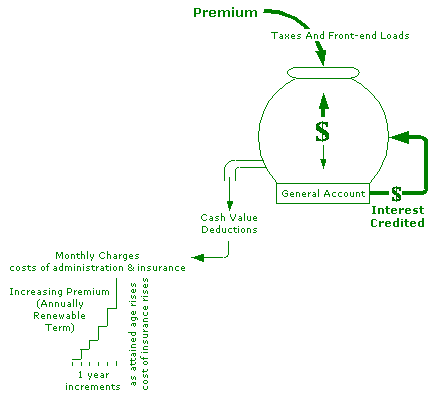

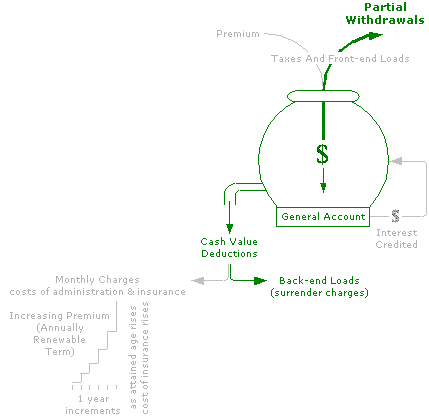

Out

of each premium deductions may be taken for such items as taxes

and expenses. The latter are the insurance company's normal

operating costs. When taken from the premium it's called a front-end

load. This reduces the amount of money entering the policy for

the cash value. The remainder of the premium is then added

to the policy cash value which is deposited in the insurance company's

general account.

Each

month charges are deducted from the cash value to pay for the

costs of administration and insurance (the annually renewable

term product). These last deductions will increase each

year as the policyholder grows older, consuming an ever larger

portion of the cash value.

Each

month, after charges are deducted from the cash value to pay for

costs of administration and insurance, tax deferred interest is

credited.

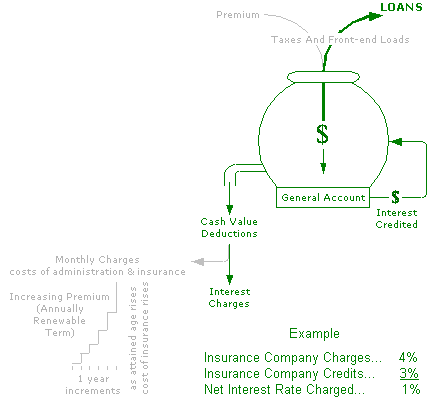

An insurance company show two different interest

rates on an illustration: the guaranteed minimum, and the "current

rate" which is based on the insurance company's investment

returns, is subject to change and not guaranteed. Cash value

growth may occur as long as the amount of premiums paid (less

taxes and front-end loads) plus the interest credited exceed the

costs of administration and insurance. But if the premiums are

not sufficient to both cover the monthly charges and allow the

cash value to grow, policy lapse may become a significant concern.

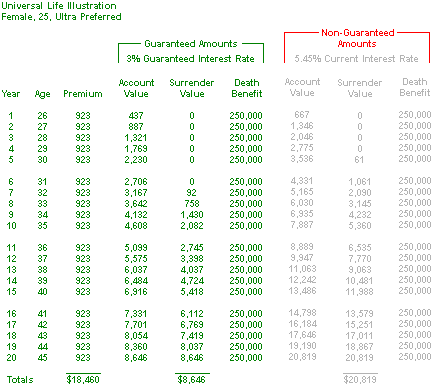

The

chart is divided into two sections, guaranteed and non-guaranteed.

Only the guaranteed values should be used in considerations, as

these are the amounts the insurance company is contractually bound

to. Typically, the non-guaranteed values reflect current

interest rates and demonstrate what the result would be if the

returns were to remain constant, a highly unlikely proposition.

Still, the chart can be useful in illustrating the concept of

how the policy will perform with a higher interest rate

For example: a quick review indicates that in the 20th year non-guaranteed

cash values will begin to exceed premiums paid.

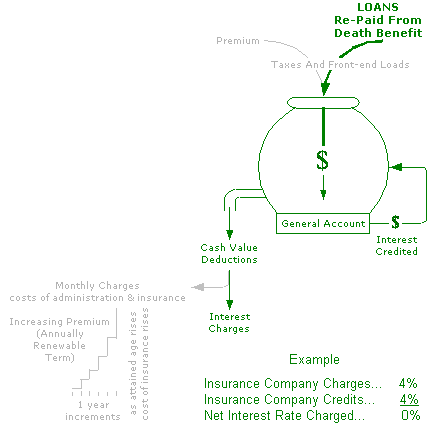

An

insurance company reserves the right to increase the cost of insurance

up to the maximum allowed in the policy. This has the effect of

reducing an insurance company's liability as the pool of policyholder

cash values are drained to support the price increase. For those

with cash value, the option is either to terminate the insurance

or increase premium payments to offset the cash value drain. For

those without cash value the option is either to terminate the

insurance or increase premium payments to keep the policy from

lapse. A no lapse guarantee may prevent forfeiture of the

death benefit, but will do nothing to preserve cash values which

will be depleted at an ever increasing pace with the combined

effects of the rising cost of insurance and attained age.

For the insurance

company, increased premium payments is an increase in income.

For

an insurance company, the amount at risk (sometimes called the

insurance element) is the death benefit less the cash value. In

addition to health, life-style and age factors the cost of insurance

is based upon the amount at risk. Cash value in a universal life

policy is absolutely vital. If the cash value has not grown quickly

there may be more insurance element at risk than was projected

and as a result the cost of insurance will be higher. If

the premium (less taxes and front-end loads) plus the interest

credited is not enough to cover the monthly charges the cash value

will be utilized to keep the policy in force. Left unchecked,

the cash value may become smaller while the insurance element

larger, then the cost of insurance will be higher and even more

of the cash value utilized to keep the policy in force.

A

no-lapse guarantee prevents policy lapse in event the cash value

is insufficient to cover the costs of administration and insurance.

Even though the policy may have no cash value, as long

as a designated premium is paid the policy will remain in force

for the length of time the guarantee is valid, as specified in

the particular policy. Thus, even though there's no cash value,

the death benefit may be retained.

Early

"super-funding" may position the policyholder to maximize

the potential of the investment portion.

Super-funding is paying the maximum permitted by law without the

policy being considered a Modified Endowment Contract: (MEC loans

and withdrawals are taxed less attractive than cash value life

insurance policies). By super-funding the cash value the

policyholder can take maximum advantage of the tax benefits of

available: tax deferred growth, income tax free withdrawals up

to premium amount paid, and increased death benefits under Option

2. The super-funded cash value can help offset increasing

premium requirements of rising cost of insurance charges in later

years. It can also be used as as the policyholder sees fit:

educational funding, supplemental retirement income or as other

needs and wants arise.

In

order to be considered for preferential tax treatment as insurance,

one of two tests must be passed, the Cash Value Accumulation Test

or the Guideline Premium / Corridor Test. Thje choice of

which test to use must be made at policy inception and can't be

changed later.

Options

are available if the policy fails the Cash Value Accumulation

or Guideline Premium / Corridor Test ...

There

are many different premiums. Each premium has a different

impact on the performance of the policy.

Building

cash value may be thought of as similar to building equity in

a home. Out of each payment deductions may be taken for

such items as principle and interest. As the loan is paid

down the equity is built up. For universal life insurance,

out of each payment deductions are taken expenses. Then,

a portion of the premium is credited to the cash value.

Just like equity in a home can be accessed, so too can the equity

in universal life insurance be accessed. The

cash value may be available through loans, partial withdrawals

or policy surrender. Also, financial institutions usually

will accept the cash value of life insurance as collateral.

Loans

may be payable either in advance or in arrears. When payable

in advance, a check for the amount of the loan is drawn, less

the first year's interest charge (hence payable in advance). Thereafter

interest is charged at the beginning of each year that the loan

remains outstanding. When interest is payable in arrears,

a check for the full amount of the loan is drawn and interest

is charged at the end of the year (hence payable in arrears).

Thereafter interest is charged at the end of each year that the

loan remains outstanding. Interest accrues daily. Any unpaid

when due is added to the outstanding balance of the loan to accrue

and compound. Left unchecked, this may result in the loan exceeding

the cash value. In such a case funds will be required to avoid

policy termination and potential tax consequences.

Loans

may be taken up to the surrender value, (cash value minus any

surrender charges), less a deduction for the costs of administration

and insurance as detailed in the policy. Usually, there

are no expenses and no front-end loads (service charges)

for re-payments. The loan interest rate and structure is

identified in the policy. Typically, an insurance company

will offer a better rate than can be obtained through commercial

lending sources. The insurance industry is unique in the

common use of interest crediting. When a policyholder takes

a loan the insurance company charges interest, but at the same

time interest is credited to the full cash value, including the

amount borrowed. The difference between the interest rate

charged and the interest rate credited is called the spread: it

is the net interest cost to the policyholder. Often the

spread is 1% or less.

Some

universal life policies may have provision for a zero interest

loan, commonly known as a "wash loan". The interest

rate charged is matched with an equal interest rate credited on

the full cash value, again, including the amount the policyholder

has borrowed. When structured correctly, a zero percent

loan allows for the cash value of the policy to be used as a source

of supplemental retirement income. The money is drawn out

as loans over a period of time. Loans do not have to be

repaid but instead can be paid out of the death benefit. Be aware

though, outstanding loans may reduce the death benefit, and further,

if not structured, correctly serious tax consequences may occur.

Consult an accountant well versed in the use of wash loans before

engaging this strategy.

Partial withdrawals (sometimes called partial surrenders) may

be taken up to the surrender value, with minimum distributions

depending on the specific insurance company and policy.

Under Death

Benefit Option 1, the face amount of the policy will be reduced

by the withdrawal amount. The face amount of the policy

remains the same under Option 2, but the the total death benefit

amount reduced by the amount withdrawn. No repayment of

the withdrawal is required. However, if the policyholder chooses

to place the amount withdrawn back into the policy, front-end

loads may be charged.

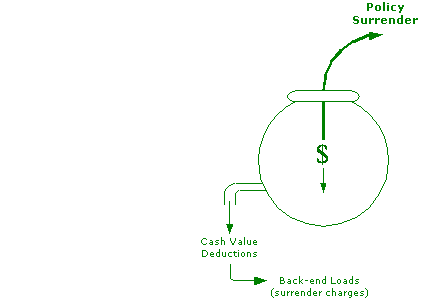

Policy

surrenders may be taken up to the surrender value, less any back-end

loads, depending on the specific insurance company and policy.

Typically, surrender charges decline as the policy is held longer.

Policy surrenders may be considered similar to selling a house.

When the owner sells a house s/he receives the equity value after

all other charges are paid.In a standard universal life product,

when a the owner surrenders a policy s/he receives the surrender

value after all other charges are paid.

Some

insurance companies offer three, but typically two death benefit

options are offered.

Request

A Quote

We're

delighted you've decided to request information through our service.

From start to finish the process takes less than 5 minutes, that's

it!

please

choose your destination

Universal Life Insurance allows a person

the opportunity to shift a portion of the burden of risk

from themselves to a large corporation. With a piece

of paper, a drop of ink and pennies on the dollar, insurance

creates cash where none existed before, usually far more

than people can accumulate in a lifetime. Further,

life insurance is the only product that provides a guarantee

to pay a specific amount at a specific time, typically

at the very time when financial resources may be strained.

And death

benefits are generally federal income tax free.

No-lapse guaranteed universal life offers several other

guarantees as well. A form of permanent insurance,

it's guaranteed never to expire, never to need renewing

and the premium never to increase. Once you've qualified

it doesn't matter how your health or lifestyle changes,

you're rates are guaranteed to stay the same. And

unlike term insurance, which has only a death benefit,

universal life premiums generate cash value. From

this cash value spring living benefits such as the potential

to use the policy as collateral, or to borrow funds with

an interest rate as low as one or even zero percent.

No other life insurance product offers a combination of

guarantees and living benefits like universal life.

But be aware this is not an inexpensive product.

Some of the factors effecting the premium include:

• your

age

• your health

• your lifestyle

• your use of nicotine

• your choice of benefits

When considering the purchase of a policy you should measure

the outlay against the weight of your assets. Life

insurance offers certain financial protection, it allows

you the opportunity to provide for your legacy with someone

elses money: namely, the insurance company's.

This

is the point at which I recommend you stop and

evaluate before proceeding any further. Unless

you have an academic interest in the understanding

of universal life insurance, further reading will

be of limited value until you resolve a few main

questions:

Do you want to preserve your assets for your legacy?

On a month-to-month basis what's really in your heart,

the cash in lieu of the protection, or the protection

in lieu of the cash?

Is your income enough to afford the cost without making

significant financial adjustments?

If

you can earnestly answer yes to these questions then we

may have a basis for moving forward. Crown Financial Services

can help you find the best policy at the best price.

As an independent, we're not limited to presenting just

one company, but can freely provide you with the resources

you need to make a sound, confident decision.

If you answered yes, then Contact

Us Today!

How Universal Life Insurance Works

There are two portions to this product: the insurance and

the cash value.

Your Money Buys

Life

Insurance and Opportunity

For

Protection

Cash

Value

Accumulation

Cash Value Accumulation Test

Used

when funding is desired is higher than the

Guideline Premium / Corridor Test allows.

A higher cost of insurance creates larger

premiums which generate a higher death benefit

in early policy years. Although there

are no premium-to-face amount ratio limitations,

the cash value may never exceed the amouint

needed to fund future contract benefits (the

net single premium).

Guideline

Premium / Corridor Test

The

default choice if none is made on application.

This test allows a policy to have more

investment orientation in the later policy

years than a comparable policy tested under

the CVA Test. Also generates a higher death

benefit in later policy years. This

is a two-part test that must be satisfied

at all times. The Guideline Premium

test requires premiums not to exceed the greater

of Guideline Single Premium or sum of Guideline

Annual Level Premiums. The Corridor Test requires

the death benefit exceed the cash value by

a percentage set forth in the Revenue Code.

Officially,

if a premium exceeds guideline tests a letter

of explanation will be sent to the policyholder

with a refund. Officially,

if a premium exceeds guideline tests and creates

a Modified Endowment Contract a letter of

explanation will be sent to the policyholder

without a refund. It is the responsibility

of the policyholder to request a refund within

a certain period of time or the premium payment

will remain the policy will become a Modified

Endowment Contract.

Realistically, there are two methods of resolving

test failure: the company may return premiums

to the policyholder to reduce the cash value

or the death benefit may be increased.

The former method may not be the optimal choice:

the test may be successfully passed one year

and then fail the next even though no more

premiums are paid. This is because the cash

value can remain level or even decrease while

the corridor percentage decreases each leading

again to failure. The

latter method is often found in policies.

In addition to correcting test failure, this

allows increased mortality charges on the

larger net amount at risk.

Guideline

Single Premium

Guideline Annual

Level Single Premium

Guideline 7 Pay Premium

Target Premium

The single premium at issue needed to fund

the future benefits under the contract using

the standards set forth in the Revenue Code.

The annual level equivalent of the Guideline

Single Premium payable until a deemed maturity

date between the insured's attained ages 95

and 100 using the standards set forth in the

Revenue Code.

The maximum premium that may be paid in each

of the first seven years after issue or material

change date using the standards set forth

in the Revenue Code.

The premium required to fund the policy at

current cost of insurance and interest rates.

Premiums above target will be applied to the

policy's cash value.

Standards set forth in the

Revenue Code include cost of insurance and

interest rate assumptions.

Death Benefit Choices

Option

1

Death benefit equal to

the policy face amount

Option

2

Death benefit equal to

the policy face amount

plus policy cash value

(premiums will be higher

for option 2 plan)

BENEFITS

(subject to limits specified

in the policy)

Eliminates

problem of future insurability: does not expire

after certain period of time and does not need

to be renewed.

Flexible premiums allow amount and timing of

payments to be adjusted.

The cash value, plus interest credited, can

be used to keep the policy active if a premium

is reduced or missed.

Interest on cash value is tax deferred.

Interest may be adjusted monthly, thus during

periods of rising interest rates cash values

may increase rapidly.

Policy loan availability.

Borrowed funds to continue

to earn interest, at a reduced rate,

even while the owner of the policy

enjoys full use of the money borrowed.

Cash withdraw availability. Policy may be surrendered

for cash surrender value.

Amount of insurance may be increased or decreased.

Death benefits are generally

federal income tax free.

DISADVANTAGES

(subject to limits specified

in the policy)

Flexible premiums may lead to under-funding

and possible policy lapse.

Without a no lapse guarantee under-funding will

result in policy lapse.

Only the minimum interest rate is guaranteed.

Using current or projected interest rate assumptions

can expose the policyholder to significant risk

if the assumptions fail to materialize.

Policy loans may reduce the cash surrender value

and death benefit.

Withdrawals may reduce the cash value and death

benefit.

Surrender charges.

Evidence of insurability may be required for

death benefit increases.

Generally, due to internal costs of the policy,

the term insurance costs more than if purchased

alone.

Cash values depletion through an

increase in the cost of the annually renewable

term product.